Table of Contents

malerapaso

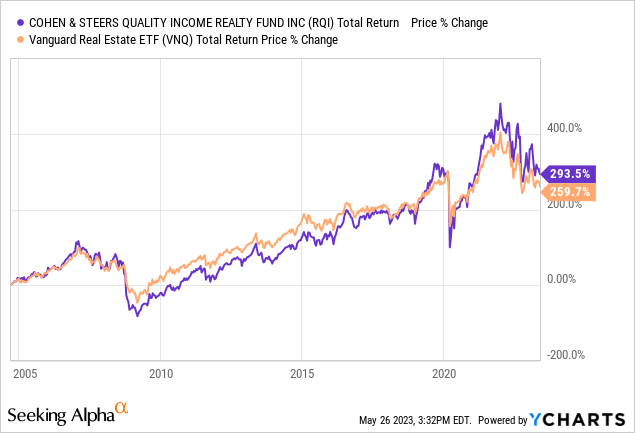

The Cohen & Steers Top quality Money Realty Fund (NYSE:RQI) is a wildly popular significant yield REIT fund. Much of its legend stems from its monitor document of outperforming the REIT sector (VNQ) about a extended-interval of time:

Nevertheless, we think that this monitor file is misleading buyers, environment them up for lengthy-term disappointment by investing in RQI. In this short article, we focus on why RQI is bound to lead to disappointing results for most if not all shareholders and then provide some option large yielding authentic estate picks that will probable supply extra satisfactory success.

Why RQI Is Poised To Disappoint

A person reason why we imagine that RQI is bound to disappoint traders over the prolonged-term is basically since its very long-term observe report is not nearly as good as it seems in the chart we just shared with you. 1st of all, if you look at the periods where REITs bought pummeled, you will discover that RQI considerably underperformed VNQ each time. The motive for this is basic: RQI – as a closed close fund – uses quite a bit of leverage. As a consequence, when REIT price ranges go up, it usually outperforms the broader REIT sector. When REIT costs drop, it commonly underperforms the broader REIT sector.

The amplifying effect of leverage is more increased by the simple fact that CEFs are absolutely free to trade at deep savings and huge rates to their fundamental NAV. As a outcome, when REITs are in favor, RQI’s share price typically trades at a greater ratio relative to its NAV, whereas when REITs are out of favor, RQI’s share cost typically trades at a broader lower price to its NAV. Eventually, this means that RQI is a very volatile instrument, negating a lot of the meant diversification added benefits that occur from holding a big fund like RQI or VNQ for REIT publicity.

Also, study has revealed that most retail buyers have a tendency to vastly underperform the broader sector for a single uncomplicated rationale: they come to be victims of their thoughts and have a tendency to market during risky sector crashes, thus locking in steep losses and oftentimes missing out on some of the strongest upward moving times that the sector encounters. As a consequence, by investing in leveraged, unstable items like RQI, odds are you are environment on your own up for long-time period underperformance. In other words and phrases: retail investor beware, buy RQI at your individual hazard and make certain that you can continue on to hold it even for the duration of violent market crashes though it is underperforming the broader REIT sector.

One more purpose why we imagine RQI is poised to disappoint traders moving forward is summed up in the knowledge of Warren Buffett:

Performance will come, functionality goes. Charges by no means falter.

When RQI may like to trumpet its interval of outperformance, the actuality of the make any difference is that with curiosity premiums having risen and possible to stay greater for lengthier at the identical time that industrial actual estate is getting disrupted like seldom just before, the fund is heading to have an progressively complicated time offering interesting returns for shareholders. This will confirm even more to be the case when you choose into account that it fees 1.34% in expenses and fees to shareholders on top rated of the fascination expenditure for its leverage.

Very last, but not minimum, when RQI’s present distribution yield of 8.75% appears to be attractive, it is important to keep in brain that its distribution may well not establish to be sustainable for the duration of a economic downturn in which some of its underlying holdings could have to lower their dividends. The higher leverage ratio on the fund may perhaps exacerbate the impacts of these prospective cuts by even extra.

Five Genuine Estate Significant Yielders To Invest in In its place

In its place of investing in RQI, we believe buyers would be better served by obtaining the adhering to substantial-yield blue chip REITs:

- EPR Homes (EPR) – an entertainment concentrated triple net lease REIT that features a superior and well-covered produce, trades at a steep price reduction to NAV, and has pretty sound lengthy-term progress possible, all backed by an expense quality harmony sheet with plenty of liquidity.

- Alexandria Serious Estate Equities (ARE) – a really high excellent lifestyle science lab house landlord that has a incredible track history of providing market-crushing complete returns, strong dividend progress just about every calendar year, and has a person of the strongest balance sheets in the REIT area. It is presently priced at a deep price reduction to NAV and must supply double-digit returns along with a lower chance profile.

- Simon Residence Team (SPG) – the primary mall and outlet center landlord that owns a perfectly-diversified and large top quality portfolio of properties. Property stage fundamentals are booming and the dividend is developing. Meanwhile, the balance sheet is one particular of the strongest in the REIT space and earns an A- credit rating score from S&P. In spite of all of this, the stock price is heavily discounted relative to historic averages and the dividend yield has soared to ~7.25%.

- STAG Industrial (STAG) – an industrial REIT with a strong stability sheet and sturdy development charges that is priced at a price reduction to NAV. For a REIT in an in-favor sector like this that also enjoys some defensive attributes forward of a recession, we assume this is 1 of the most no-brainer buys in the REIT place these days.

- W.P. Carey (WPC) – previous but not minimum, WPC delivers one particular of the greatest all-all over risk-adjusted large yields in the marketplace today, combining a quite secure and rising 6.3% dividend generate with a pretty defensive portfolio that is more and more focused on mission-significant triple web lease industrial properties. Also, it derives most of its rent from leases with inflation-joined contractual hire escalators, and its BBB+ credit score score gives it an eye-catching cost of capital.

Investor Takeaway

RQI certainly has an alluring expenditure scenario: a observe document of outperforming VNQ more than the long-term, a superior regular monthly distribution, and the guarantee of protection that arrives from a properly-diversified portfolio managed by a highly regarded fund supervisor.

That explained, buyers will need to keep in head that RQI’s management charges are rather superior and that the higher generate and periods of outperformance are mostly owing to the very significant leverage ratio that the company has assumed. When this has served RQI well in the previous through durations of low fascination premiums and financial prosperity, we are now in a higher curiosity fee and declining financial ecosystem. As a result, buyers are setting on their own up for a most likely wild roller coaster journey in RQI and the exploration indicates this will guide most retail investors to underperform over time as they allow for their feelings to get the very best of them during market place crashes.

As a outcome, we would caution retail traders to do some thorough self-examination right before obtaining RQI to make sure that you have the psychological makeup to maintain it through volatile durations. Also, we assume investors will do just as properly – if not much better – in excess of the extended-phrase by forgoing the large costs and risky leverage of RQI and just develop on their own a portfolio of blue chip REITs like people described in this article. That is what we have completed at Significant Yield Investor, and it has served us extremely effectively.

More Stories

A Fresh Approach to Home Buying: Essential Tips Every Modern Homebuyer Should Know

The Family Bonding Moments That Begin When You Own a Lake House

The Popularity of Hidden Halo Engagement Rings in London