Table of Contents

For the past several years, the real estate market has been a twisted game for homebuyers. The ability to secure the perfect home constantly eludes them, as they get crushed by institutional buyers with all-cash hammers, pricked by sellers wielding their power to overprice homes, and sucked into a pipeline of precarious financing.

Stefan Peterson | Credit: LinkedIn

However, an emerging business model is helping homebuyers win the game — similar to the effect of a single Super Mushroom that transforms Mario from a dwarf to a looming giant; power buyers are imbuing everyday buyers with the capital needed to crush the competition and seal the deal.

“What power buyers do is make the buyer effectively a cash buyer, or as some folks have pointed out, they turn any buyer into an iBuyer,” Zavvie co-founder and Chief Data Officer Stefan Peterson said of the model’s flagship cash backing and buy-before-you-sell offers. “I think that’s a neat way to look at it. Imagine it — I’m just humble Stephen Peterson out in the housing market trying to buy a house, but now I’ve got the muscle of an iBuyer to do it.”

“We couldn’t have come up with a better way to describe this class of companies,” he said, giving kudos to real estate analyst Mike DelPrete who coined the term. “Why that term is a good one is because [power buyers] really increase individual buyers’ power in the marketplace to go out and buy a house.”

The table of contents:

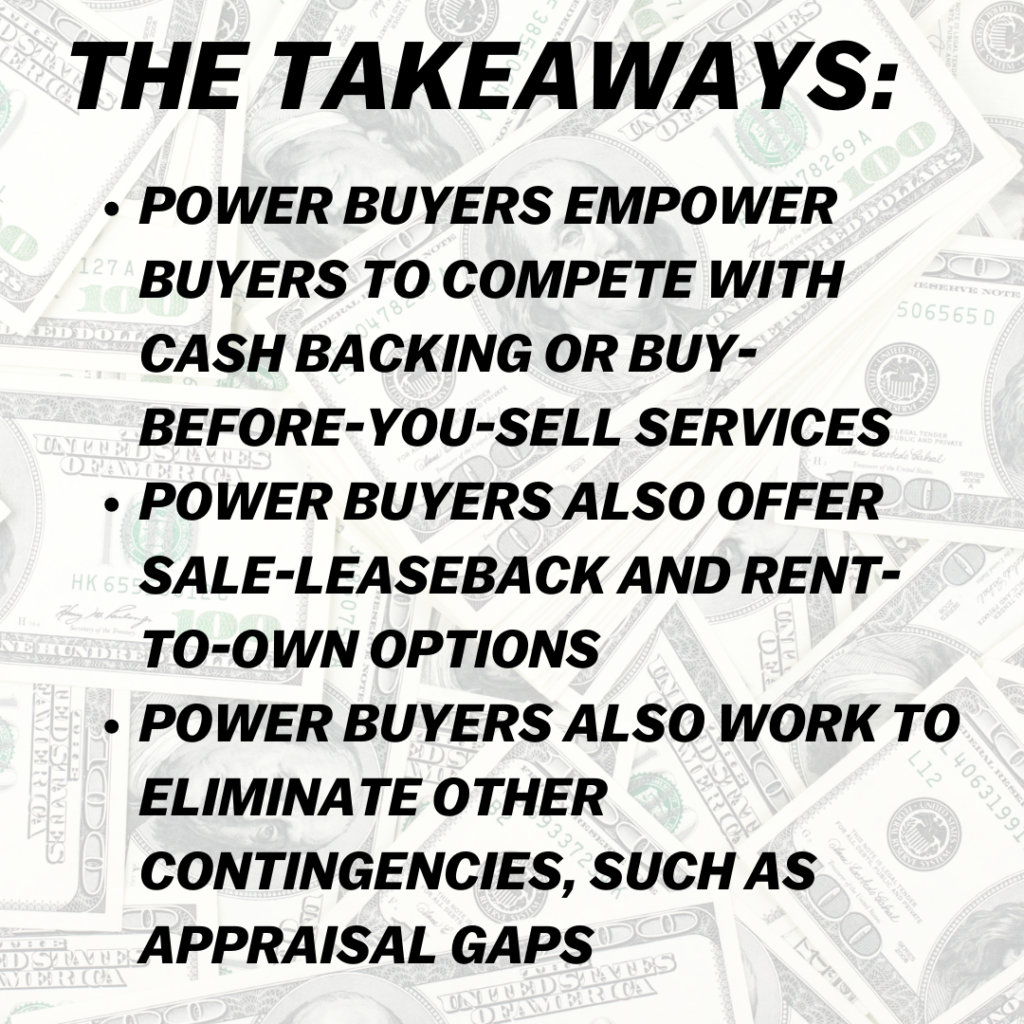

What do power buyers offer?

As Peterson noted, power buyers help homebuyers compete in the marketplace through two primary services: cash-backed offers and buy-before-you-sell. Both services, he and several others said, solve two main issues homebuyers face in today’s market — the ability to compete with iBuyers, institutional buyers, affluent buyers who are flush with cash and navigate the trickiness of being a seller-turned-homebuyer.

Here’s how the majority of cash offers work:

- To get a cash offer, a homebuyer must complete a qualification process that confirms their creditworthiness and provides a budget. Once approved, the homebuyer chooses the home they want to purchase, and the power buyer purchases the home on the buyer’s behalf with an all-cash offer to a seller.

- From there, the buyer may be required to provide an earnest money deposit or pay a flat-rate transaction fee. Power buyers who offer mortgage and title services will often waive the transaction fee if a buyer decides to finance their purchase with them as well.

- The buyer can move into the home immediately while they secure a mortgage to repurchase the home from the power buyer.

- The buyer will often pay a prorated rental fee for the time they stayed in the home before closing on their mortgage.

Meanwhile, buy-before-you-sell options take cash offers a few steps further:

- For homesellers-turned-homebuyers, they’re able to complete a similar process through a buy-before-you-sell service.

- Buy-before-you-sell services are an alternative to bridge loans and help this segment of homebuyers expertly navigate two simultaneous transactions.

- Homebuyers will complete the same steps as a homebuyer who is looking to simply secure cash backing, except they’re given an extended rental timeline to sell their previous home and secure a mortgage for a new home.

- The power buyer can help them sell their home on the open market with home prep services and the guidance of an in-house agent.

- If they’re unable to sell their home on the open market within a certain number of days — usually 180 — power buyers will purchase the home themselves.

Tim Cooke | Credit: LinkedIn

“I think [power buyers] solve ‘the chicken and egg issue,’” Flyhomes for Agents Director of Sales Tim Cooke said of the importance of power buyer services, particularly buy-before-you-sell. “I own a home and in order for me to buy a new home, I need to release the equity from my old home, but I can’t buy the new one before I sell the old one, and I don’t want to sell the old one until I know for sure that I’m going to be able to buy the new one,”

“That’s especially important in the current environment, but that issue has always been around,” he added. “What a power buyer does is step in and say, ‘We’ve got you. Don’t worry.’”

While cash backing and buy-before-you-sell services are the bread and butter of most power buyers, sale-leasebacks and lease-to-own services have their own important part to play on the smorgasbord of buyer services.

Sale-leaseback programs enable homeowners to sell their homes to a power buyer in order to access a portion of their home’s value in cash. The buyer will continue to rent their home with the option to repurchase or release the power buyer to sell the home on the open market, which enables the homeowner to get another payout, minus the power buyer’s purchase price.

Jared Kessler | Credit: EasyKnock

A leader in the sale-leaseback space, EasyKnock CEO Jared Kessler said sale-leasebacks provide similar benefits to cash backing by enabling homesellers to essentially back themselves through their home equity. “What really excites me about our role in the marketplace is that by giving the consumer access to their hard-earned home equity, we’re empowering them to be a better buyer,” he said.

On the other hand, lease-to-own companies, which are lesser-known as homeownership accelerators, offer the same benefits as cash backing services with a much longer repurchase timeline. These companies serve homebuyers who are on the cusp of purchasing but have issues with financing, such as securing a mortgage or saving a robust down payment.

After performing their own qualification process, lease-to-own power buyers purchase a home on a homebuyers’ behalf and rent the home back to them for as much as 24 to 36 months. During that time, the company will put a portion of the monthly rent into a down payment fund, and provide financial guidance.

When the homebuyer reaches their financial health and down payment goal, they’re able to purchase the home from the power buyer. Or, they can walk away and pocket the savings for a future purchase.

Cyril Berdugo | Credit: LinkedIn

“We’re a power buyer for the segment of the United States that can’t get a mortgage right now,” Landis co-founder and co-CEO Cyril Berdugo said. “If you’re able to buy a house on someone’s behalf and make it affordable for them to buy back by setting a fixed repurchase price, what you’re effectively doing is making the product completely independent of macroeconomic cycles, whether markets go up or down.”

“[Lease-to-own companies] provide price certainty to the client,” he added of how he and his competitors empower buyers.

Outside of those four main offerings, power buyers are quickly responding to consumer needs by developing ancillary services that address other pain points in the homebuying process. For example, Ribbon launched an appraisal protection service in April, with Knock following up with a similar service for Knock GO (Guaranteed Offer) in October.

Wei Gan | Credit: Ribbon

Ribbon co-founder and Chief Tech Officer Wei Gan said there’s plenty of opportunities for power buyers to expand past cash offers and begin crafting solutions that eliminate other hang-ups in the transaction process — such as appraisals and inspections — to create certainty.

“A lot of the innovation in real estate tech and proptech around the transaction has been around this core problem of certainty in the transaction,” he told Inman. “The way that we think about [our product development] is how do you remove all the contingencies in a transaction?”

Gan said contingencies revolve around financing, inspection, appraisal or home sale itself, and power buyers are positioned to remove those contingencies to create a seamless process for buyers and sellers alike.

“I’ll give you that maybe as a sneak peek to the future of power buying, at least from Ribbon’s point of view,” he added in reference to the company’s upcoming inspection service.

Real estate analyst Mike DelPrete said power buyers have only scratched the surface of what’s possible, and it’s important for industry professionals and consumers to expand their view of what this model contributes beyond cash offers and buy-before-you-sell.

“I needed something to call these companies,” DelPrete said of coining the term “power buyer.” “I don’t think it’s fair for them to be lumped into this category of just cash buyers or bridge loan companies.”

“If you’re thinking of these companies like that, you’re missing the game. These are companies that are building something from the ground up for buyers,” he added while noting power buyers are positioned to shake up the mortgage industry, as proven by an average mortgage attach rate of 70 percent. “We’re in the early innings of seeing what power buyer actually does.”

Additional resources:

Who’s currently in the power buyer space?

Mike DelPrete

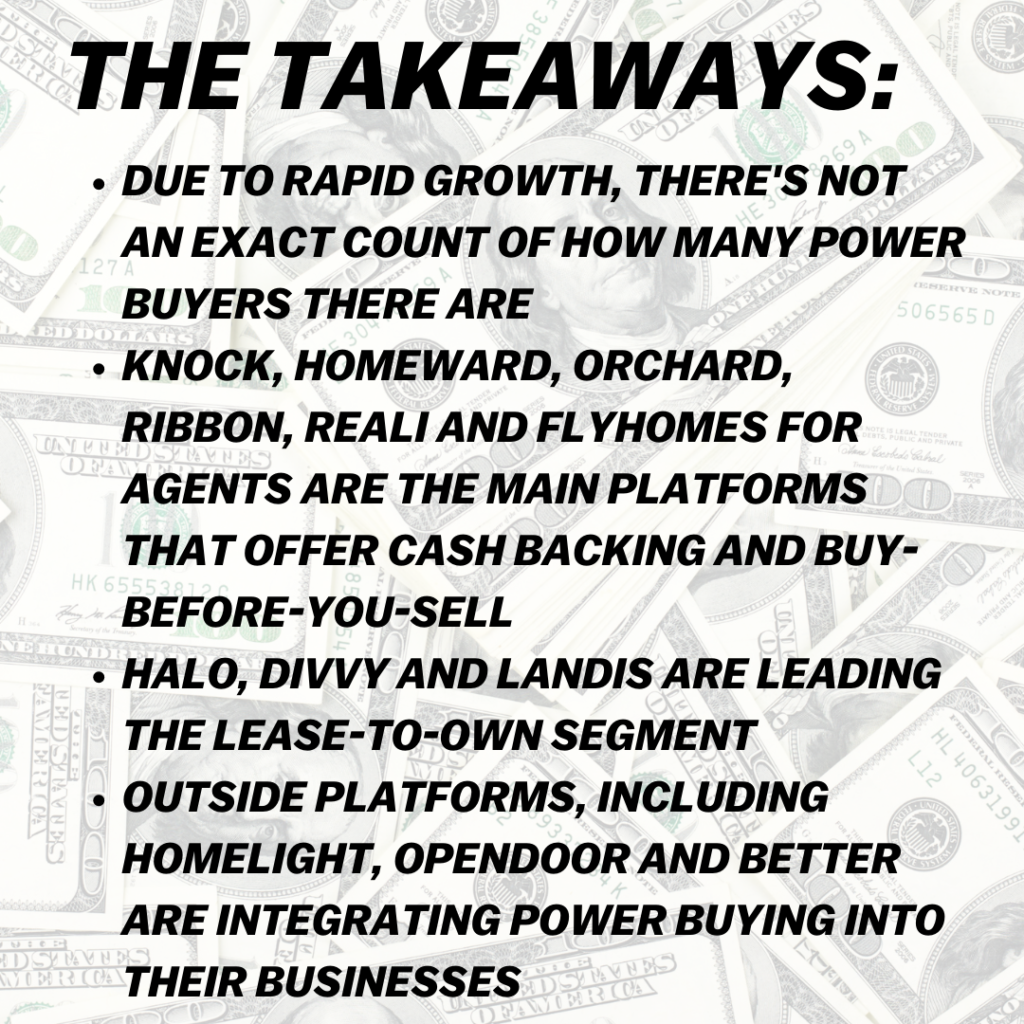

The power buyer field is like the Wild West, with a steady stream of new entrants coming to place their stake in untapped markets or homebuyer segments. With power buyers only serving between 12,000 to 15,000 homebuyers in 2021, DelPrete said there is equal opportunity for established companies and startups to gain market share.

“There’s a lot of different flavors out there,” he said while noting he’s unsure of the total number of power buyers. “But as we’ve seen with iBuying, it starts small and it grows fast — the number of power buyers is growing exponentially, the amount of money they’re raising is growing exponentially, the amount of customers they’re serving is growing exponentially.”

DelPrete highlighted Knock, Homeward, Orchard, Ribbon, Reali and Flyhomes for Agents as some of the main power buyers, all of which offer cash offer and buy-before-you-sell services with varying funding methods for homebuyers (conventional loan, equity advance, buy-then-repurchase), transaction fees (flat fee or percentage fee plus closing costs) and ancillary features (appraisal protection, inspection guarantees, home-sale prep).

“I don’t want to pick winners,” said DelPrete, who serves as an advisor for Homeward. “But the companies, like the ones [I] mentioned, that have [capital and reach] will be the operating system for power buyer services that agents and brokers will begin to offer.”

Knock

Sean Black | Credit: Knock

Arguably the largest power buyer with operations in 69 markets, Knock offers two flagship services, Knock GO (Guaranteed Offer) and Knock Home Swap. The platform powers both services with conventional mortgages they underwrite and guarantee to fund, so buyers can make a contingency-fee offer and skip the process of repurchasing their home from Knock.

Knock GO offers a guaranteed closing date and appraisal gap protection, while Knock Home Swap includes an equity advance that enables homebuyers to cover a down payment, $25,000 of home repairs coordinated through Knock’s home-prep concierge service, and mortgage payments on the old home while it’s on the market. With Home Swap, Knock also promises to purchase the home if it doesn’t sell within six months.

Homeward

Tim Heyl | Credit: Homeward

Austin-based Homeward serves homebuyers in eight cities across Texas, Georgia, Colorado and Arizona. To get a Homeward Cash Offer, homebuyers must go through an approval process that sets their budget. Once a seller accepts the buyer’s Homeward-backed cash offer, homebuyers must pay an earnest money deposit, schedule an inspection and sign mortgage disclosure documents.

Homeward will close on the home within 14 days, which enables buyers to move into their new abode. While they secure the mortgage to purchase the home back from Homeward, buyers will be charged a prorated rental fee that’s due at closing. The company’s buy-before-you-sell option works in a similar fashion, with homesellers-turned-homebuyers having a six-month rental option while they sell their previous home.

Orchard

Court Cunningham | Credit: Orchard

Orchard, the latest real estate company to reach unicorn status, focuses on the buy-before-you-sell segment of the market with two options, Move First and Buy & List. With Move First, homesellers can unlock up to 90 percent of their home’s equity to pay down their mortgage and provide a down payment on a new home. For those who need the power of an all-cash offer, they can qualify for cash backing through Orchard’s Offer Boost.

Meanwhile, Orchard Buy & List follows a traditional transaction process with a licensed Orchard agent guiding homebuyers through selling their old home and securing a bridge loan and mortgage to fund the purchase of a new one. This option is for buyers who are comfortable with a longer timeline, Orchard said, and want to save on fees.

Homebuyers can also access Orchard’s other offerings, including Orchard Dashboard, Orchard Insurance, and Orchard Concierge — a home prep service with no upfront costs.

Ribbon

Shaival Shah | Credit: Ribbon

Four-year-old Ribbon, which Inman tech guru Craig Rowe dubbed the industry’s “first hybrid fintech-proptech application,” offers an array of services for consumers and industry professionals alike.

RibbonBoost provides homebuyers with cash backing and appraisal gap protection. If a homebuyers’ financing falls through, they can transition to RibbonReserve. With RibbonReserve, Ribbon will purchase a home on their behalf and allow them to move in with a prorated rental fee. Homebuyers then have six months to secure their financing, after which they’ll purchase the home from Ribbon for the same price.

Ribbon also offers RibbonRescue, which enables buyers under contract to use RibbonReserve at a higher fee, and guaranteed closing service for sellers. To access any of these services, consumers must first invite their agent to the Ribbon platform.

Reali

Oren Zeev | Credit: Reali

San Mateo-based real estate startup Reali offers cash backing and buy-before-you-sell services specifically for California homebuyers. Both services work like most power buyers in the space, with Reali financing the purchase and then enabling buyers to repurchase a property once they’ve secured financing. All homebuyers will have the support of a dedicated local agent and transaction coordinator or cash offer specialist.

Reali also has a home search platform and offers mortgages through Reali Loans.

Flyhomes for Agents

Flyhomes for Agents is the latest addition to Seattle-based company Flyhomes’ array of subsidiaries, Flyhomes Brokerage, Flyhomes Mortgage and Flyhomes Closing.

Tushar Garg | Credit: Flyhomes

Flyhomes cash offer and buy-before-you-sell funding mechanism is a short-term loan that’s given to buyers to make a contingency-free offer. That short-term loan is then refinanced into a long-term loan with a 30-to-45-day closing timeline for cash offer buyers. For buy-before-you-sell clients, Flyhomes will also apply the proceeds from the sale of the old home toward the down payment on the new home.

Consumers who use a Flyhomes Brokerage agent to facilitate their transaction won’t pay a commission since Flyhome agents work on a base salary and transaction bonus. Cash offer buyers will pay origination, desktop appraisal, title, escrow, and other settlement costs, which can be partially waived if they also use Flyhomes Mortgage.

Buy-before-you-sell clients will pay a broker commission, a transfer or excise tax (if applicable), any seller closing costs, and a daily holding (e.g rental) fee. Also with buy-before-you-sell, if the home doesn’t sell in six months, Flyhomes will purchase the home unless the client wants to keep it on the open market.

Tom Egan | Credit: LinkedIn

These main companies scratch the surface of what’s available, with established companies such as HomeLight, Opendoor and Better wading into the power buying and new entrants such as UpEquity blasting their way in. There’s also a small grouping of lease-to-own companies — namely Divvy, Landis and Halo — that offer the same benefits as cash backing services with a much longer repurchase timeline and down payment assistance so aspiring homebuyers can stairstep their way into homeownership.

“We provide a path to homeownership for folks that are not ready to buy, not able to buy or just prefer the convenience of a product that offers them the time to do it on their own, at their own pace,” Divvy Chief Financial Offer Tom Egan said of how lease-to-own services are also beneficial for qualified homebuyers who need more flexibility due to changing work and family obligations. “The use case has sort of expanded over time, so we’ve started to think about our business as sort of enabling homeownership more broadly.”

Additional resources:

The power buyer tipping point

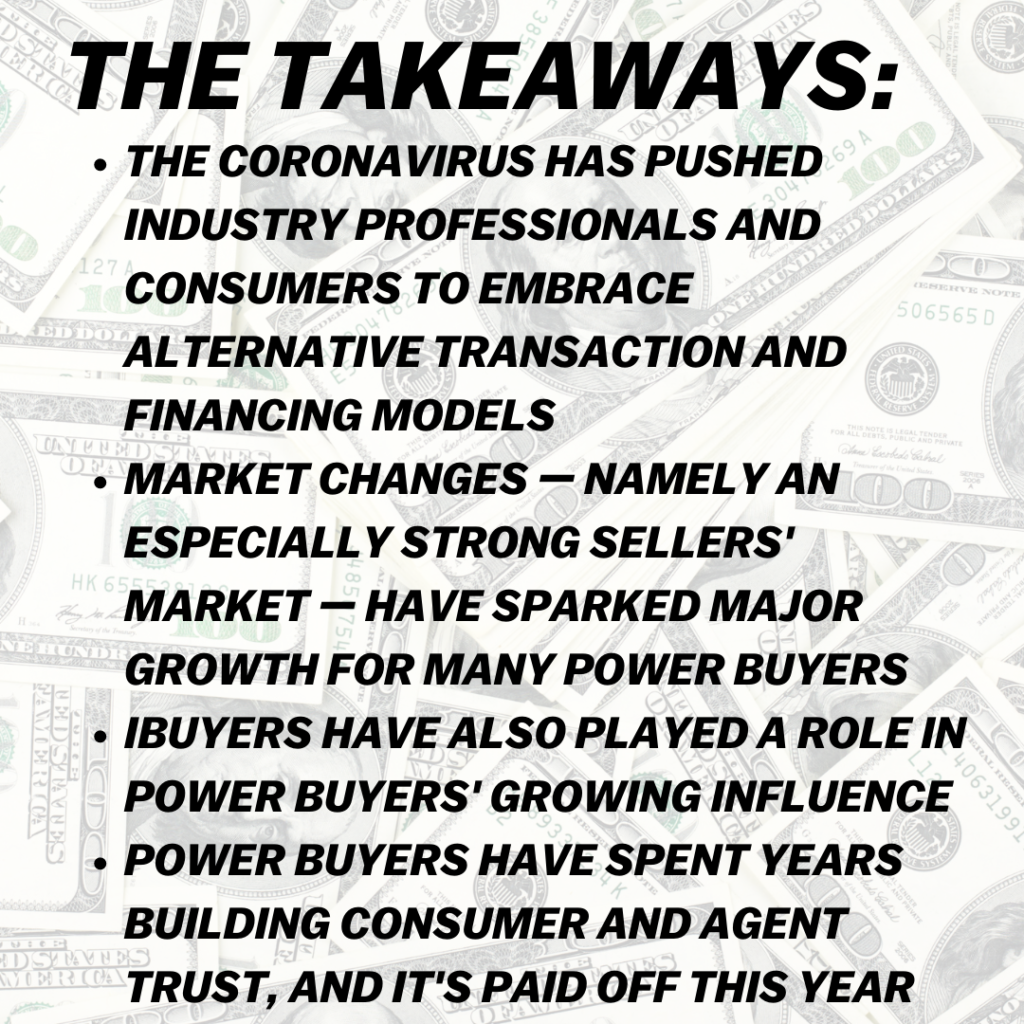

The transaction revolution started well before the coronavirus; however, as many real estate professionals and experts have noted, the pandemic accelerated innovation and pushed adoption rates to record highs as agents and consumers grasp for any advantage in an unpredictable market.

“The pandemic caused a massive home inventory shortage and really accelerated consumer adoption for any service that made it easier to secure a good home,” Homeward founder and CEO Tim Heyl said. “Power Buyers used to work hard to convince agents and buyers we are trustworthy, but today we are fortunate to be able to just prove it.”

Those years of trust-building have enabled power buyers to put the pedal to the metal in 2021, with companies reporting enviable financing rounds, launching new services and bolstering current ones, experiencing record growth, and getting a headstart on audacious expansion plans for 2022.

“Homebuyers really look to their agent for who to trust and what to do — I’m really grateful to say great agents now have a lot of trust with Homeward and some other companies like us,” Heyl added. “That trust is only increasing with time.”

Zavvie co-founder and Chief Data Officer Stefan Peterson said the boost in adoption rates also comes from agents who understand or are beginning to understand their survival is based on being an advisor and seizing the middleman spot — even as some real estate companies seek a direct-to-consumer business model.

“These different solutions, they’re wonderful, they’re great companies, but they’re not representing a client. That’s just not what they do,” he said. “It’s becoming an urgent necessity to [become] a modern agent or a modern broker, and what I mean by that is, you’re an agent who is bringing all of these different options to the table is just part of what you do as an agent.”

“Agents need to be proactively bringing all of these options to their clients because these [options] are good for clients and clients are going to hear about them,” he added. “If agents don’t bring their clients these options, clients are going to go to these options on their own without an agent, and I don’t think that’s what is ideal.”

David Sandmann | Credit: Halo

On the lease-to-own side of power buying, Halo founder and managing partner David Sandmann their tailwinds have come from agents and mortgage lenders who are trying to help homebuyers overcome financial hurdles, which may have been exacerbated by the pandemic.

“A lot of times when we hear from lenders, it’s because somebody is near qualified,” he told Inman. “So [lenders] will come to us and say, ‘I don’t want to just turn this person away and I’d like to give them an option because I know that they’re not that far from actually getting a mortgage.’”

Sandmann also said lenders have reached out to help homebuyers who were pre-qualified, but due to a longer homebuying process with multiple failed offers, by the time they got to closing changes in their finances — mainly credit — caused them to lose the deal at closing.

“By the time they close, they find out at the closing table that something’s happened on their credit and that now they can’t actually close and they’ve got earnest money down on the house,” he explained. “They’ve gone through the blood, sweat and tears of actually getting an offer accepted and getting to the finish line, and something has popped up on their credit report that’s keeping them from closing.”

Beyond market conditions and mindset shifts, Gan said iBuyers have helped pave the way for power buyers to grow more efficiently, thanks to the work they’ve done creating familiarity about alternative transaction and financing models on a broader scale.

“The reality is there’s always some wind in the market that allows a startup to take off, right? It’s always some bit of preparation [meeting] luck, and the luck is often a market change,” he said of Ribbon’s humble beginnings in 2018. “We were a seven-person team with less than $5 million in funding, and the way that we often got off the ground, honestly, is when the iBuyers came to town.”

As iBuyers rose in prominence, Gan said professionals who’d “slammed the door in our faces” came racing back and asking for presentations about how they could use Ribbon to help their buyers compete. “They said, ‘Hey, we need your help because when we go to presentations, we need a solution to show my seller, why they shouldn’t just go with an iBuyer,’” he said. “Off the backs of [those conversations], buy-before-you-sell was born.”

Gan and several other sources said industry professionals, in general, have come to trust power buyers more than iBuyers because power buyers, from the beginning, have relied on real estate agents, in-house or otherwise, to facilitate a cash offer or buy-before-you-sell deal.

“We’ve been empowering, not disrupting the real estate ecosystem,” Gan said. “What we have done is provide these lenders, brokerages, and so forth, with cash offer solutions to help their customers and their agents be able to win the homes that the homebuyers love.”

“I think real estate agents, only trust companies that don’t take a portion of their commission and put them in the center of the transaction,” Landis co-founder and co-CEO Cyril Berdugo added. “We are working with real estate agents and making real estate agents our allies. We’re not playing a zero-sum game.”

Additional resources:

What lies ahead for power buyers?

Although no one has a crystal ball to exactly predict the future, Peterson said power buyers’ robust growth and conversion rates are a reliable indicator of where they’ll be in the next three to five years.

“Power buying solutions are applicable to far more buyers and sellers who are going to buy,” he said. “We’re seeing conversion rates in the 30 percent range and in some cases, we hear they’re quite a lot higher. It’s related to the fact the main challenge in the market right now is not selling a house, it’s buying a house.”

“For some sellers, iBuyers are a great solution. Just full stop on that,” he added. “When you look at overall conversion rates with iBuyers, they’re at the 5 to 6 percent range. For a majority of sellers, just selling your house on the open market is preferable.”

Furthermore, Peterson said the value proposition of power buyers will hold up in a variety of markets — a concern that’s been highlighted with iBuyers, especially in light of Zillow Offers’ dramatic end.

“We at Zavvie have thought about this, and we’ve talked about it,” he said. “A consumer considering a power buyer model, what they’re after is really convenience it provides, and that is going to hold up whether it’s more of a buyers market, or more of a seller’s market — the power buyer solution is still going to help.”

“Even if it’s a buyers market, you’re still going to have an advantage by being a cash buyer in a buyer’s market,” he added. “Is [the advantage] a little bit less? Sure. Is there a little bit less benefit to being able to buy and then sell later? Yeah. But it still helps a fair amount to have that service behind you and simplify things for you.”

DelPrete echoed Peterson and said the power buyer model does a better job of incentivizing agents and consumers to buy into the process. “Just because your neighbors sell their house to Opendoor doesn’t mean you’re any more or less likely to be incentivized to sell your house to an iBuyer,” he explained. “The opposite is true for power buyers.”

“The more people that use that service, the more incentivized people who are not using the service will be to sign up so they’re on an even, competitive playing field when they’re looking to purchase a home,” he added.

The power buyers Inman interviewed for this story were all bullish about their long-term prospects despite slowing market activity, continued supply constraints, rising mortgage rates, buyer fatigue and unknown circumstances, like the pandemic, that could arise and cause the real estate industry to dramatically shift course again.

“The reality is, we haven’t had a down market in in real estate since the [rise of the] iBuyer. We haven’t had a real market crash, and no one wants that,” Gan said. “But then what that means is the jury the jury’s still out, right? We don’t know exactly how resilient the iBuyer model is going to be, and frankly, because of that we don’t know exactly how resilient the power buyer model is going to be.”

However, he said the simple fact that power buyers don’t have to hold onto thousands of homes — although all power buyers do offer a six-month purchase guarantee that ensures they will have some stock — means they’re less susceptible to the whims of the market.

“We’re brokering a trade between a buyer and a seller, right? We’re not buying a home and then waiting for it on the open market and then trying to sell it at a profit,” he explained. “What that means is for every single home that Ribbon buys, we already have a buyer that we’re helping buy a home.”

“Having a buyer there means all the difference, right?” he added. “We’re not trying to flip on the open market — The reality is our model is predicated on a small fee that either the lender or the buyer pays or the agent pays at the closing, and we’re not marking up the price at all because that’s not our profit center.”

If it seems like power buyers are simply boasting, Peterson and DelPrete said industry professionals only need to look at who’s steadily moving into the power buyer space. “You see more big companies are great companies getting into this, it signals to everybody that, hey, power buying is really a legitimate path,” Peterson said of Opendoor and Better’s foray into cash-backed offers. “It’s validation for the space.”

DelPrete said it’s not just a good idea for iBuyers and mortgage companies to dip their feet into power buying, but it’s actually key to their long-term resilience.

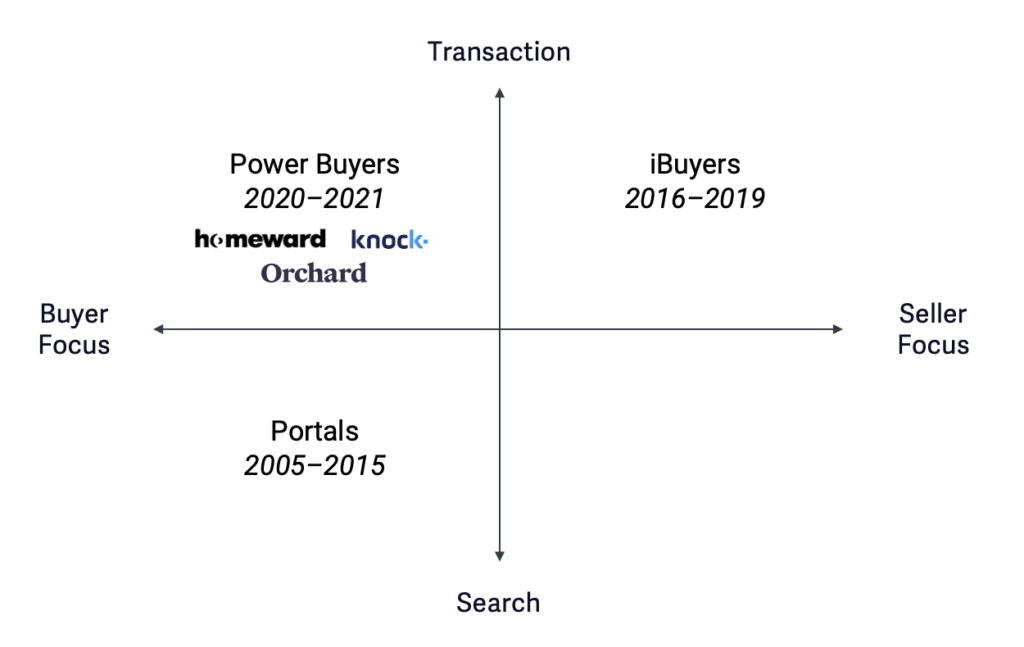

DelPrete’s transaction grid.

“So you have iBuyers, well, really specifically Opendoor going into this space as well, which makes a lot of sense,” he said. “If you imagine a chart with services that are close to the transaction for sellers and services that are close to the transaction for buyers, iBuyers are going to be in that seller quadrant, and then power buyers are going to be in the buyer quadrant.”

“It turns out that one of the biggest business benefits for the power buyers is really high mortgage attach rate,” he said while noting iBuyers without power buying services have really struggled to achieve that same attach rate. “So if you’re Opendoor it makes sense to go into [power buying] because you want to get more people using your mortgage.”

Both men said there will be some consolidation as the model picks up speed; however not enough to where current and incoming power buyers should be concerned about being cannibalized by a bigger company. If anything, Peterson, DelPrete and others said, the increased competition will incentivize companies to stay ahead of the curve and push the envelope on what services they offer.

“IBuyers and Power Buyers are similar in that they both are seeking to create better moving experiences by taking on risk that consumers have had to take in the past,” Heyl said. “While Homeward doesn’t have plans to get into the iBuying space, I do see both types of companies expanding their solutions over time.”

“What we both have in common is that we are consolidating services to create more seamless experiences — that’s a great thing for the consumer, and with some Power Buyers [like Homeward] it’s a great thing for agents too,” he added. “There may be brand consolidation at some point, but right now the market is so big and no company has yet tapped into any significant share, so I don’t see it happening very soon.”

Lastly, Berdugo said power buyers will continue to succeed if they keep two things in mind: the agent and the consumer.

“Agents are still going to be at the center of the transaction, and clients are going to reach out to their agents for options and alternatives,” he said while noting the majority of consumers still rely on agents for their transactions.”The only thing that power buyers need to do is educate the agent in the best way possible so the agent can make the best decision possible for their client.”

Additional resources:

Email Marian McPherson

More Stories

A Fresh Approach to Home Buying: Essential Tips Every Modern Homebuyer Should Know

The Family Bonding Moments That Begin When You Own a Lake House

The Popularity of Hidden Halo Engagement Rings in London